摘要: Improving High-Frequency Trading: Using Artificial Intelligence, Machine Learning and Software Defined Radios to Break Down Technological Barriers.

摘要: One step back, two steps forward. That was the path for automation, algorithms and artificial intelligence applications in fixed income trading over the past few months.

摘要: Algorithmic trading has proliferated across global FX markets over the past decade. Today, roughly 20% of the institutional foreign exchange trading volume is now executed through algos. FX algo usage is following that of the equities market - where algos currently account for more than half of all equity trading volume. So what’s behind all this algo growth?

摘要: Executing trades in the financial market has been made extremely accessible. With a few hundred $ and an internet connection you have the whole world under your thumb. This makes it seem that trading is a simple way of making big bucks. Being profitable in the market however demands a lot more than just entering trades, even if you happen to obtain accurate signals.

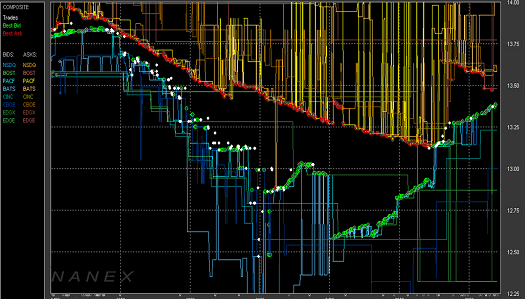

摘要: I hesitated using the word “tick” in the title of this post, lest potential readers think I am writing yet another post on tick sizes.[1] But I assure you, this post has absolutely nothing to do with tick size.